There’s a good chance that banks generate more data per transaction than Netflix does when streaming a movie. All digital interactions—customer interactions, payments, risk assessments, regulatory reports—provide information that can radically change how financial institutions function. Most banks still rely on monthly and quarterly reports for decision-making, thus not on real-time data, which is a key differentiator between market leaders and followers.

Data analytics in banking is essential as we approach 2026. It’s not just the adoption of new tools; it’s a change in how a bank perceives and understands customers’ needs, the risk landscape, and the value propositions it offers.

Why Banks Need Data Analytics in 2026?

The banking environment of 2026 will shift even more from what it was only five years ago. Customers expect increasingly personalized, immediate services, while market volatility continues to expand and deepen. Regulators continue to move the goalposts, and the pressures resulting from the growing complexity of these factors are the new normal for data analytics in banking and financial services.

In these circumstances, the value of data services in banking becomes urgent and unassailable. See, data-forward banks survived the market volatility and seized opportunities while their competitors were still formulating their plans. Analytics-enabled banks discern customized services and unarticulated client needs far in advance of their competitors. They identify and mitigate risks long before they become problematic.

Numbers demonstrate the magnitude of this transformation. The data analytics in banking market

In the next decade, the banks that succeed will view data as the bedrock of modern banking, rather than an ancillary output of the banking process.

Now, let’s see how banks use data analytics.

Enhancing Experience with Personalized Services

Competition for unique value primarily depends on service delivery and client experience. Big data analytics services, pricing, ancillary services, and core banking service configurations are increasingly similar across banks.

However, big data analytics in banking industry applications can reshape service relationships. Rather than every contact being a transaction, analytics recognizes and anticipates a client’s unmet need and shapes service delivery. The very meaning of service is transformed from a banking transaction to guidance.

Examples:

- Customer-centric analytics are exemplified in AI tools at Bank of America, especially in Erica, the virtual assistant. Beyond analyzing the customer’s request, Erica prescribes analytical steps designed to help them save, spend, and improve their overall financial position.

- Citibank also incorporates analytics into its omnichannel customer experience strategy. The bank ensures a seamless customer experience across mobile apps, ATMs, and branches by allowing customers’ real-time data to flow freely across all integration points. Citibank’s automated systems predict customer requirements and service needs and offer customized services with precision at the predicted payment moments.

Improving Risk Management and Compliance

Risk has always been a banking constant, and its parameters have always changed. Before, banking relied on periodic assessments and historical patterns to quantify potential risk. Now, modern risk banking entails immediate detection and real-time response to threats.

By using data analytics in banking and finance, providers can create sophisticated financial forecasting systems that warn of potential losses. These systems predict and prep responses by continuously monitoring and analyzing transactions, customer behaviors, and market conditions.

Example:

- At DBS Bank in Singapore, the advanced AI-powered risk analytics systems demonstrate efficacy. They analyze data to pinpoint potential fraud and prevent losses from fraudster attacks. Since AI analyzes data more quickly and accurately than traditional systems, it helps prevent losses by detecting fraud in time. But the system’s active learning algorithms continuously optimize the bank’s fraud detection algorithms.

Improving Efficiency and Decision-Making

Just like any other industry, bank operations processes consist of activities that yield varying levels of efficiency, customer satisfaction, and resource utilization. Such important information is usually trapped in departmental silos or summarized in overly cursory reports that miss critical operational details.

In the banking sector, predictive analytics applications transform operational data into actionable insights. Using AI development services, banks can now adjust processes, resource allocation, and even real-time operational analytics to identify and eliminate resource allocation bottlenecks.

Examples:

- The Bank of New York Mellon Corporation is another example of operational improvement driven by analytics. After implementing banking analytics, the Corporation drastically reduced processing time and achieved higher accuracy in account-closure validations. These improvements show that it is possible to operationalize efficiency gains and sustain capabilities over time.

- An example of resource utilization improvement in the same analytics-driven approach is the new digital Bank in Abu Dhabi. It implemented operational analytics and integration tools that increased resource utilization and made operations faster, safer, and more productive.

What is Data Analytics in Banking Industry

Banking institutions process millions of transactions and manage sophisticated risk portfolios while also adhering to strict regulations. In this business milieu, data analytics in banking industry has gone from being a niche capability to a core strategic function.

Successful banks operate with an integrated analytics approach, focusing on three pillars:

- real-time decision-making for customer engagements

- risk estimates

- operational changes on the go

Types of Data Analytics

Data analytics in banking industry occurs at four levels, each addressing a different type of insight and decision.

- Descriptive analytics. Descriptive analytics seeks to understand past performance, workflows, and finances.

- Diagnostic analytics. This type of analytics seeks to uncover the reasons behind the financial performance trends.

- Predictive analytics. Predictive analytics estimates potential fraud risks, predicts customer churn, and loan defaults.

- Prescriptive analytics. By analyzing multiple scenarios, prescriptive analytics supports optimal decision-making and delivers desired results.

Key Data Sources in Banking

Banks have access to enormous slices of data. Making the most of them is the first step toward advanced analytic capabilities. The most important data sources include the following:

- Transactional data: this is the most basic source of data, comprising millions of activities, payments, money transfers, and investments. By analyzing the transactions, spending patterns, financial health, and unusual behavior, it can be detected.

- CRM data: data such as customers’ demographics, interaction histories, products owned, and customer communications are valuable to banks for segmentation, targeted campaigns, and churn prediction.

- Data on credit and risk: information pertaining to individuals’ credit repayment history and income trends is internal data, as are models and the risk of lending to individuals and businesses.

- Market data: the investment banking division is constantly monitoring real-time market data to make trade decisions, manage portfolios, and provide advice on mergers and acquisitions.

- Social and unstructured data: these data sources help provide qualitative value to the analytical process. It helps banks analyze trends, understand customers, and monitor sentiment.

Benefits of Data Analytics in Banking

The use of data analytics in banking

Strategic Resilience to Market Volatility

The financial markets are constantly changing due to interest rate fluctuations, regulatory changes, and global economic conditions. Banking analytics offer relevant tools to help people understand the chaos. Good banks and other organizations combine historical and real-time data to build sophisticated scenario models. This is especially relevant for stress-testing models to understand the impacts of potential market shocks on their strategic plans. Proactive data forecasting allows bank management to shift strategies on the fly in response to changing events.

Revenue Growth Through Better Customer Experience

By building a complete profile of a customer from mobile apps, transaction data, and service interactions in their systems, data analytics in banks can decipher customer needs and behaviors.

This knowledge supports predictive analysis down to the “next best action”—anticipating a customer’s next requirement, be it a home loan, investment, or savings. JPMorgan Chase offers leading data analytics in digital banking. Chase Media Solutions provides customized cashback offers and turns standard banking into a lucrative experience for millions of its customers. Such incredible value to consumers strengthens loyalty and opens completely new avenues for profit.

Profit-Driven Operational Models

While profitability hinges on efficiency, many banks still face profit erosion from inefficient legacy processes. Data analytics in banking sector provides insights into organizational inefficiencies. By tracking service and process cycle times and determining the frequency of ATM maintenance and servicing, inefficiencies can be pinpointed in real time. This facilitates decision-making on the provision of service at a lower operational cost. For instance, advanced data management solutions enabled the Bank of New York Mellon to improve account closure processing times, proving that analytics increases profitability.

Safer Banking with Intelligent Risk Protection

Banking fraud detection systems have, in the last couple of decades, been weighed down by rules that are often too rigid to be responsive and user-friendly. Cyber fraud detection systems that leverage surveillance, big data AI, and real-time analytics, as reflected in customers’ transactions, are the new systems banks are offering.

Banking Governance with Data-Based Decisions

The more dispersed the data is, the more sophisticated the analytics are for predicting compliance with regulations such as the Dodd-Frank Act, Basel III, and GDPR. Automated systems to monitor compliance gaps shift the effort from manual activities and the oversights that can carry significant organizational penalties.

Data Analytics Use Cases in Banking

Data analytics in the banking industry is designed to enhance customer satisfaction, support risk assessment, drive business growth, and improve process efficiency.

Customer Experience and Personalization

In today’s business landscape, providing exceptional customer service is the competitive market differentiator. By implementing big data analytics in banking, institutions can advance from basic service offerings to tailored ones. With the ability to construct definable customer profiles and use omnichannel data banks, it can deploy NBA and NBO models that leverage predictive analytics to determine which services and products customers are likely to need next.

Capital Allocation and Yielding Returns

Correct data analysis provides visibility and enables the allocation of resources to achieve a better return on investment. Investments across different products and customer segments allow for more efficient tracking and allocation. The data enables banks to run scenario analyses and to model various stress tests across a range of interest and currency shifts.

Scenario modeling fosters greater flexibility and resilience. However, building models requires specialised technical knowledge. So, if you’re wondering why do companies outsource IT, this is one of the reasons. To build a high-quality model that yields returns, you need a team of professionals with rich experience and a technical background. However, if you decide to hire an external team, you should also educate yourself on the risks of outsourcing software development.

Fraud Prevention and Risk Management

Fraud prevention is always an ongoing battle and a costly issue. With the development of advanced big data analytics in banking industry, financial institutions can shift from a reactive to a proactive approach to fraud detection. Artificial intelligence-powered algorithms can track and monitor transactions. They can see in real time which transactions exhibit parametrically suspicious behavior.

Consistent Operational Efficiency

Process optimization is another area where the value of big data analytics in banking sector is evident. Banks can monitor key performance indicators to analyze their data and track the cost-to-income ratio, return on assets, and process cycle times as they navigate and identify system inefficiencies. Digitally powered process mining can use machine learning to autonomously identify system bottlenecks.

Barriers to Using Data Analytics in Banking

Challenges of digital transformation in banking make it hard for organizations to become data-driven. Older banks, in particular, face technical, regulatory, and systemic issues.

Data Quality and Standardization

An analytics model is only as good as the data it is given. When it comes to banking, data comes from a variety of sources, leading to inconsistent formats. Such fragmentation can skew insights and lead to poor decision-making.

To remedy this, banks need to develop comprehensive data-integrity mechanisms. These can include automated data cleaning and validation, clear data lineage tracking, and routine audits. But this is more than a technical challenge. It’s an organizational problem — and the solution is to change the culture. Banks need to define data ownership and develop a common understanding of data standards and governance models that can be applied consistently across all divisions.

Integrating Legacy Systems

Many banks still use legacy core banking systems built for stability rather than the real-time processing of large data volumes needed today. Those legacy systems can be incompatible with modern analytics tools, and the data within them is often locked away in silos. It’s a costly and risky move to replace those systems.

In this sense, the best practice is to use hybrid cloud banking or to add cloud-native building blocks and APIs on top of the legacy infrastructure. This permits a bank to mine data and augment a system without undergoing a wholesale system replacement. Middleware solutions, centralized data warehouses, or data lakes can similarly be leveraged to aggregate data from multiple sources and establish a consolidated layer for analytics.

Regulatory Compliance

Globally, the banking industry faces the most stringent regulations. For example, the Dodd-Frank Act, PCI-DSS, and GDPR control how banks acquire, store, and handle customer information. Such regulations are not constant, and banks must be prepared for changes. For effective data governance, banks must embed ‘compliance by design’ into their data processes, implement automated compliance monitoring, and ensure continuous collaboration among the technology, legal, and compliance teams.

Organizational and Human Factors

Analytics technology is just one part of the puzzle. Significant changes to an organization’s culture are also necessary. Human barriers commonly include resistance to change, low levels of data literacy, and confusion as to what data can do. To address this, banks must provide training and required resources to all employees and leaders. It is also necessary to demonstrate useful, value-adding applications of data analytics and to develop an analytics support infrastructure that fosters an analytics culture.

Strategic Implementation Risks

Data maturity has its own risks at the strategy level. The costs at the start for analytics platforms, custom integrations, and team training are an upfront outlay. There are also significant cybersecurity risks when centralizing large amounts of sensitive customer data.

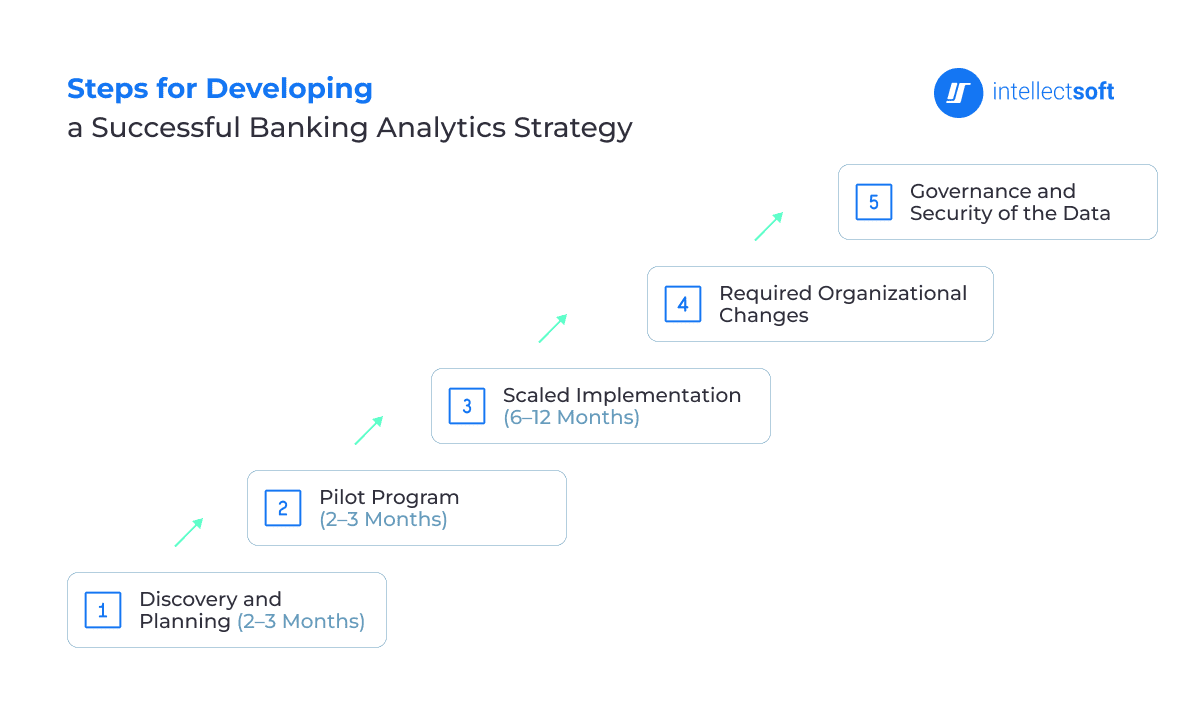

Steps for Developing a Successful Banking Analytics Strategy

Deploying big data analytics in banking market should be strategic, balancing legacy constraints and future aspirations.

Discovery and Planning (2–3 Months)

Begin by inventorying existing systems. Map them and identify data silos, with an outline of data quality assessment. This phase will also identify lower-effort, higher-reward potential use cases that demonstrate early value. Define success criteria and target ROI benchmarks. At this stage, you could benefit from IT consulting services to identify the critical processes that need patching.

Pilot Program (2–3 Months)

You should test your approach in a controlled environment. In this case, it is best to go after a high-impact use case– fraud detection, credit risk modeling, and customer churn prediction. Running a pilot in this environment gives you an opportunity to validate your assumptions, refine your models, and identify undiscovered gaps before a full deployment. It will also build internal confidence. When stakeholders in the business see the pilot yields results, they will support a larger deployment.

Scaled Implementation (6–12 Months)

At this point, you are in the expansion phase. It’s now time to interlink analytics functions across departments, integrate them into the core banking systems, and hand them to frontline employees. This stage of the cycle demands unceasing refinement and adjustment as models will drift, and shifts in data sources will require new analytics. Successful banks are those that treat analytics as an ongoing, living, evolving system rather than a one-off initiative.

Required Organizational Changes

Technology is not adequate by itself. You need the right people—statisticians, data engineers, business analysts who can merge the numbers with the underlying strategy. Many banks avoid filling this gap by using outsourcing software development services. Lastly, change management is essential. The use of analytics alters decision-making processes, requiring buy-in from leadership at all levels, including branch and frontline staff.

Governance and Security of the Data

Banking analytics processes large amounts of sensitive data and information because of the nature of the business. Once the data leaves the organization, a breach can result in losses, fines, and long-lasting reputational harm. Building data architecture that includes privacy is essential, as is automated compliance checking. Legal teams and tech teams need to collaborate on the data flow, who accesses it, and the retention period.

The Future of Data Analytics In Banking

The future of analytics is moving from reporting the past to real-time analytics. This also means moving from process analytics to predictive tools to real-time decision-making. The levels of banking analytics sophistication will continue to increase, as will the associated risks. The banks that consider predictive analytics a core competency rather than a mere side project will likely set the standards for the future of small business banking.

The Functions of AI and Machine Learning

Banking industry technology trends, such as advances in AI and machine learning, have transformed the analytical process from simply recognizing patterns in datasets to predicting data trends. For instance, HSBC employs AI-fraud prevention systems that assess transactional and behavioral patterns, detecting potential losses before they occur. Also, JPMorgan Chase developed a machine learning platform, Athena, that enhances the bank’s forecasting and risk management across its various portfolios.

Real-Time Analytics and Its Implications

Modern analytics systems provide real-time data, enabling banks to perform proactive rather than reactive functions. When a transaction is flagged as fraudulent, the bank can act in real time to freeze the account and prevent losses. Blockchain in banking industry is another great technology that helps make transactions secure and transparent.

Open Banking and API-Based Ecosystems

Although open banking frameworks compel banks to share customer data via APIs, this may appear to be a threat, but it will unlock amazing opportunities. With the right analytics, banks can acquire third-party data, such as fintech app usage, e-commerce transaction histories, and other cross-merchant data outside the banking industry, to use alongside their own data to create and refine customer profiles.

How Intellectsoft Helps Banks Leverage Data Analytics

Building data analytics is often resource-intensive. However, Intellectsoft can help you compress timeframes, reduce risks, and achieve rapid, concrete results.

Our Expertise in Data Engineering and AI Solutions

Intellectsoft offers custom financial software development services

With our data science services, you can improve operational efficiency and gain predictive analytics and automated processes, helping you achieve the desired outcome.

Why Partner with Intellectsoft

There are a few compelling reasons why you should choose Intellectsoft for your data analytics needs:

- Proven Track Record with Global Brands: Intellectsoft has years of experience delivering to global brands and Fortune 500 companies, including Ernst & Young, Jaguar Land Rover, and Eurostar. Our solutions have enabled these enterprises to utilize data for informed decision-making and operational excellence.

- 360-Degree Approach: Intellectsoft operates on a full-scale model—from ideation to post-release maintenance, offering a smooth process across all stages.

- Top Tech Talent: Intellectsoft harbours experienced developers well connected to industry niches and blockchain software development, enabling financial companies to derive data analytics solutions that are imaginative and effective.

- Effective Workshops: Intellectsoft offers sessions to sculpt and hammer out ideas and data visualization services, allowing financial firms to test their ideas at low risk before executing holistically.

- Background in Data-Driven Solutions: Our work with Ernst & Young, to name one, demonstrates our ability to position clients as thought leaders by leveraging data analytics to drive smarter investment decisions.

By choosing Intellectsoft, you will work alongside an established, client-centric partner with the technical chops to turn your data into actionable insights.

How does Intellectsoft manage cross-border data privacy compliance?

Intellectsoft applies ‘privacy by design’ policies, with automated compliance monitoring, data masking, and integration of technical and legal cross-border compliance tools designed to align with GDPR, CCPA, and regional banking privacy rules.

What obstacles do banks encounter when trying to apply analytics?

Old technology was not made for real-time analytics. Analytics are not integrated across separate bank divisions. Regulations. Issues with analytic talent recruitment. Cyber threats. Costs of analytics, especially for regional banks. Failure to deal with the issues described above will lead to ‘hope’ as a strategy, which is likely to fail to deliver results.

What is the price of a complete banking analytics solution?

Costs can range from $100,000 to $1,500,000, depending on the bank’s size, the technology it uses, the level of integration required, and the number of staff. Mid-size banks tend to have higher costs relative to the value of analytics, and these analytics add value by reducing fraud-related expenses, boosting customer loyalty, and speeding up loan processing.

Source link